The Practice of 2036

3 Predictions for the Next Decade of Healthcare Practices

For most of the last 75 years, practice ownership followed a familiar arc. You graduated, joined or bought into a business, built a patient base, worked a busy but sustainable schedule, and eventually sold to a younger partner and retired comfortably. It was one of the most reliable paths to becoming a respected local business owner with strong income, real autonomy, and a decent work-life balance.

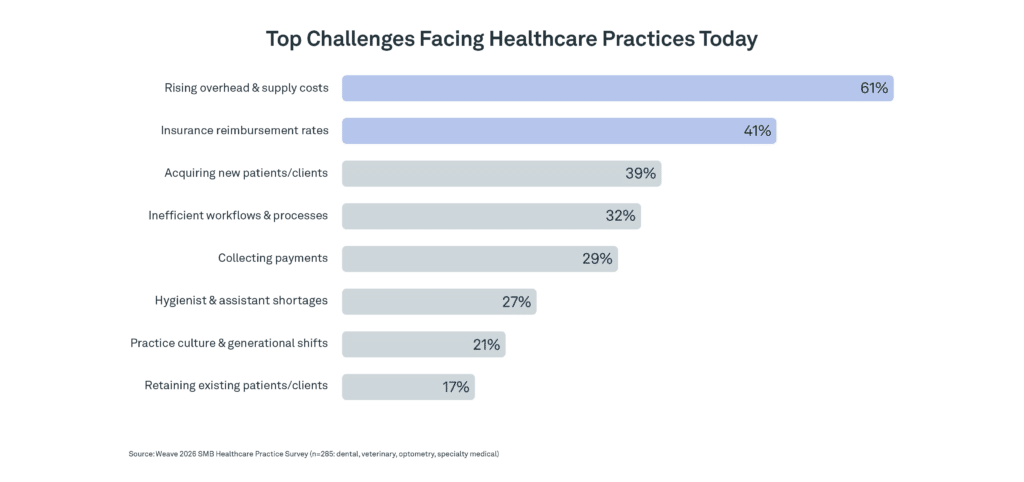

That arc is increasingly steeper. Margins have compressed across dental, veterinary, optometry, and specialty medical practices. Reimbursement keeps sliding while labor, supplies, and equipment get more expensive. Teams are worn out from doing more with fewer people, tighter schedules, and higher patient expectations. And already, AI has moved past the headline phase and is starting to impact the industry.

Dentistry, the vertical we know most deeply, tells the story in plain numbers. A decade ago, a practice owner could sustain a profit margin above 30%,1,2 earn north of $200,000 a year,3 and work three or four days a week.3 Today, the average margin is near 22%,4 median provider income has fallen to $175,000,3 and half of dentists report three years of declining insurance reimbursement. At the same time, their costs have risen on every line.5 Recent graduates carry nearly $300,000 in school debt into that math.6

Meanwhile, the ownership landscape keeps shifting under everyone’s feet as more care is delivered by group practices every year. In dentistry, roughly 82% of the country’s 147,000 practice locations remain independently owned, but the balance has been moving toward multi-location groups for a decade.7 The same pattern is unfolding in veterinary, optometry, and specialty medical.

Solo practices aren’t going away. They will, however, be competing in a market increasingly shaped by organizations with scale.

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

The industry knows change is coming. The harder question is what it will look like when it arrives. We’re making three predictions about the future of your practice that are relevant whether you run one location or 300:

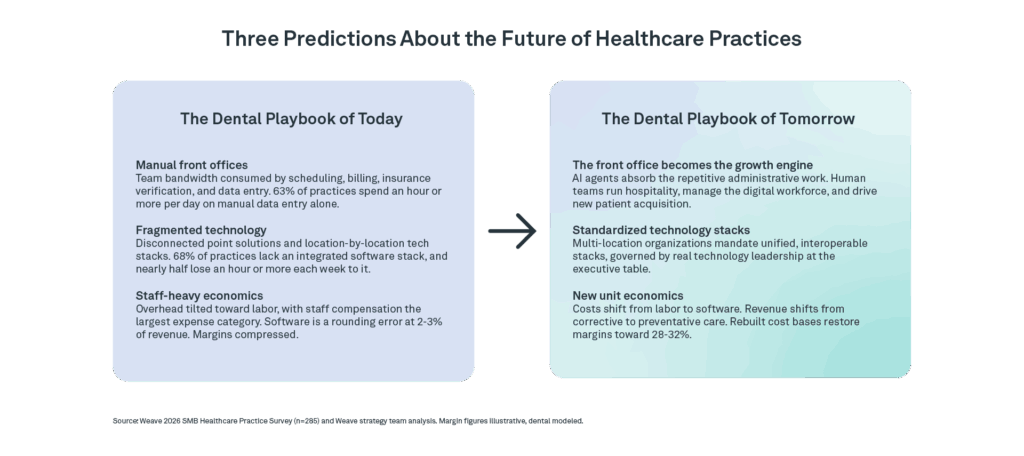

- Your front office will become your growth engine. AI agents will absorb the repetitive administrative work, and your human team will shift to the things machines can’t do: hospitality, judgment, and growth.

- Standardizing your technology stack becomes nonnegotiable. For multi-location organizations, a fragmented stack stops being a quirk and starts being the single biggest drag on profitability.

- The unit economics of your practice will change. Overhead transitions from labor to software, revenue shifts from corrective to preventive care, and the practices that adapt early will run at structurally higher margins.

9. Weave Strategy Team Internal Analysis

How We Got to These Predictions

Weave has spent nearly 20 years building software for small and midsize healthcare practices. Today, more than 40,000 locations across dental, veterinary, optometry, and specialty medical run on our platform, and we process over a billion patient interactions every year.9 That volume compounds: over more than a decade, it adds up to billions of calls, texts, and voicemails, and everything they teach about how practices actually run. We talk to practice owners, office managers, and group-practice executives every single day. When the front office breaks, we hear about it first.

Our strategy team synthesized 10 years of industry trends, interviewed more than a dozen operators, clinicians, investors, and executives across the practice landscape, and surveyed more than 280 practices across dental, veterinary, optometry, and specialty medical about staffing, technology, and financial pressure.8 We also drew on third-party research from the ADA and its Health Policy Institute, the AMA, PitchBook, McKinsey, Bain, BCG, Gartner, Anthropic, and others.

Prediction 1: Your Front Office Becomes Your Growth Engine

Today’s practices are drowning in paperwork, administrative logistics, and patient follow-up, leaving even the best employees strapped for time, focus, and energy for patients. But it doesn’t have to be this way. By harnessing AI in the right ways, you can help people do what they do best without the distraction of manual workflows. Imagine this instead:

The Practice of 2036

It’s a Friday night in April 2036. Audrey is out with friends when she feels a sharp pain in one of her molars. In 2026, she would have toughed it out until Monday, called her dentist during business hours, and hoped for an opening. Instead, she texts Dr. Jones’ office from the restaurant. Within seconds, the practice’s AI receptionist responds. It checks the schedule, finds a next-morning cancellation, confirms the emergency appointment, sends intake forms, verifies insurance, and texts a payment link for the co-pay. All of it after hours, all of it over text.

When Audrey walks in the next morning, still in pain, the administrative work is already done. She enters a quiet lobby and gets a warm greeting from Danika at the front desk. Because an AI agent handled the intake, Danika isn’t racing through a checklist. She has time to answer questions and put Audrey at ease before she ever sits in the chair. In the operatory, AI drafts clinical documentation in real time, and imaging software flags an adjacent area worth monitoring, catching something that might have slipped by on a more chaotic day. Afterward, the AI receptionist sends Audrey a visit summary and follow-up instructions, books her next cleaning, and checks in a few days later to see how she is recovering.

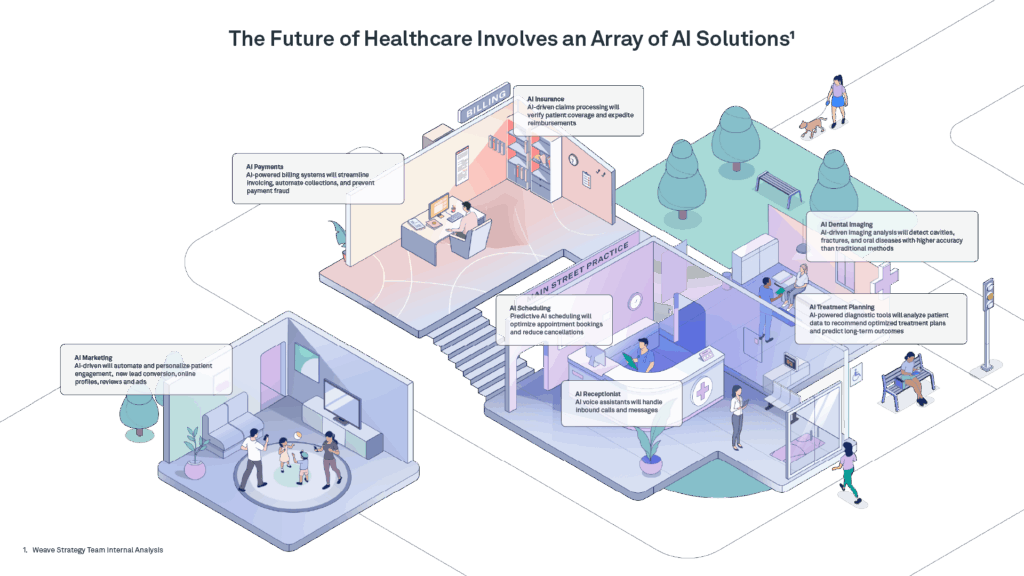

Swap the molar for a limping golden retriever or an overdue eye exam and the scene plays the same way. The scenario isn’t all that futuristic. The building blocks are already here. AI scheduling, digital forms, automated insurance verification, ambient clinical documentation, and automated patient communication are flooding the market. There are more than 90 AI receptionist solutions available in the U.S. alone, even before you count the dozens of point solutions aimed at clinical and administrative workflows.9

8. Weave Strategy Team Internal Analysis

Why This Is Happening Now

The rise of automated front desk workflows didn’t happen by chance. It’s an answer to three forces that have been besieging the front desk for too long.

1. The staffing crisis isn’t going away, and it’s expensive.

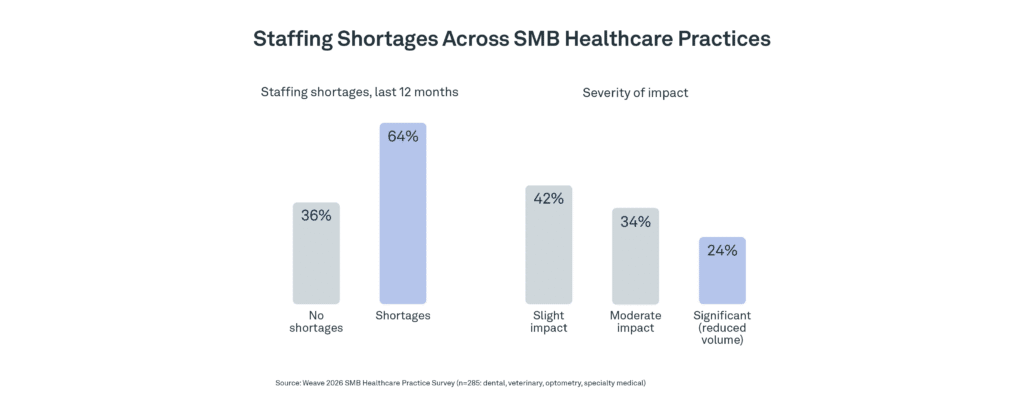

The front office has long been one of the most labor-intensive roles in healthcare: scheduling, insurance verification, intake, billing, payment collection, and recall campaigns, all layered on top of face-to-face patient care. Staff compensation is the single largest expense category, accounting for more than 40% of practice overhead.10 In Weave’s 2026 State of Healthcare Pulse Survey of practices across dental, veterinary, optometry, and specialty medical, 63% experienced staffing shortages in the last twelve months, and roughly a quarter say shortages are forcing them to reduce patient volume. Hiring takes two to three weeks in the best of circumstances, and for about one in 10 practices, it takes more than two months.8

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

2. The busywork is enormous.

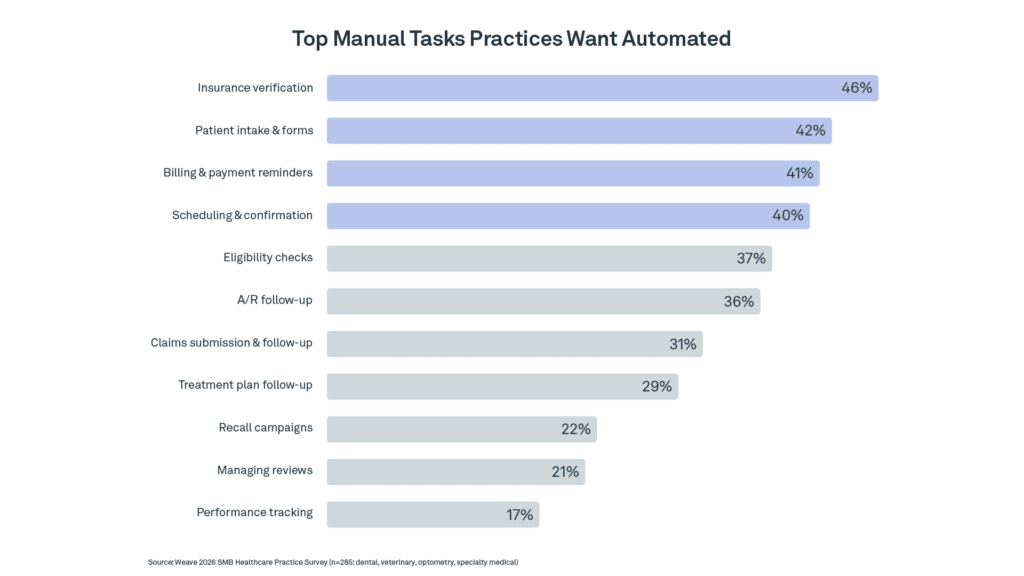

In that same survey, 63% of practices spend an hour or more per day on manual data entry alone, and 13% spend four hours or more. The tasks practices most want automated are exactly the ones AI already handles well: insurance verification (46%), patient intake and forms (42%), billing and payment reminders (41%), and appointment scheduling and confirmations (40%).8 For a group with 20 locations where front office staff average 90 minutes a day on manual data entry, that’s more than 9,000 staff-hours a year lost to work that never helps a patient face to face. Recovering just half of it represents over $112,000 in annual labor value.8,9

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

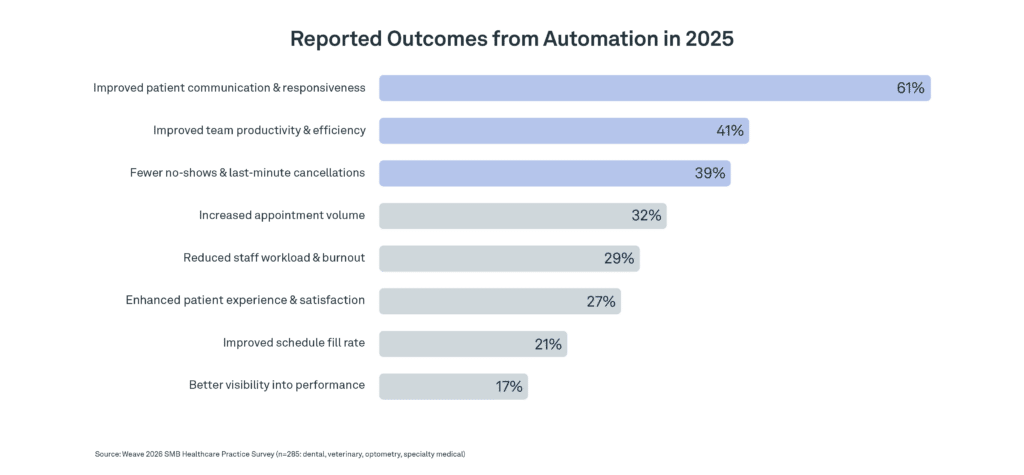

Practices that have started automating are already seeing returns: 61% report improved patient communication and responsiveness, 41% report better team productivity, and 39% report fewer no-shows and last-minute cancellations.8

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

3. The technology finally works.

AI models can now reliably perform over 60% of routine cognitive tasks: the rules-based, repeatable, highly standardized workflows that account for the lion’s share of front office work.11,12 Without addressing this, you’re stuck in an endless logistical bottleneck. Or, as Dr. Cindy Roark of Sage Dental put it, “You can’t continue to grow unless you figure something else out. And I look at agentic AI as the big unlock.”12

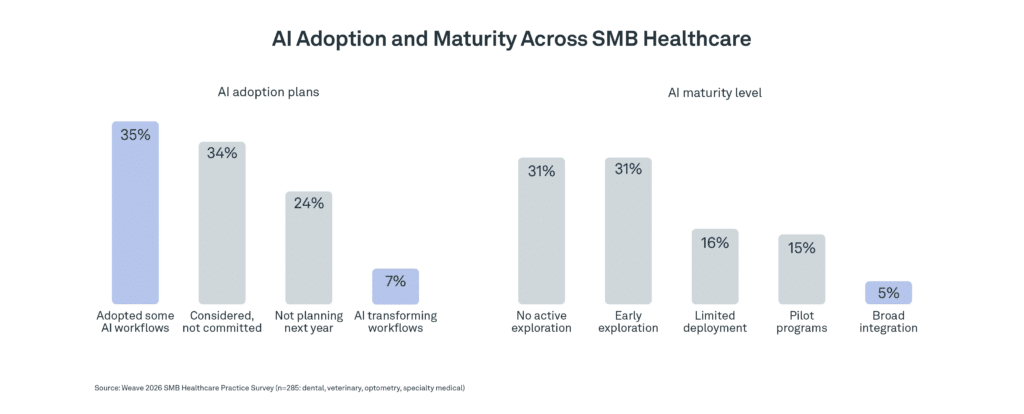

The result is a front office team that actually grows in size over the next decade, but the work will shift from humans managing manual workflows to humans managing a roster of AI agents that handle repetitive tasks: scheduling, intake, verification, billing follow-up, recall, and reactivation. Across SMB healthcare, 2 in 5 practices have already adopted AI in some form, though maturity remains low. A full 82% say AI hasn’t meaningfully changed their staffing needs yet, but that simply tells you exactly how early we are. Healthcare has always adopted technology cautiously for good reason. Adoption won’t happen all at once. It will start where the value is clearest and the workflows are easiest to define. That means the administrative layer is affected first.8

You can't continue to grow unless you figure something else out. And I look at agentic AI as the big unlock.

Dr. Cindy Roark, Sage Dental 12

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

What Your Human Team Does Instead

But AI workflows don’t mean that human work doesn’t matter — or that it’s totally replaced. This is the part that gets lost in the automation conversation: as machines take on more of the work, your people matter more than ever. The value that used to be spread across a stack of administrative tasks is consolidated and streamlined, but human skills like judgment, warmth, and inquisitiveness will be mission critical.

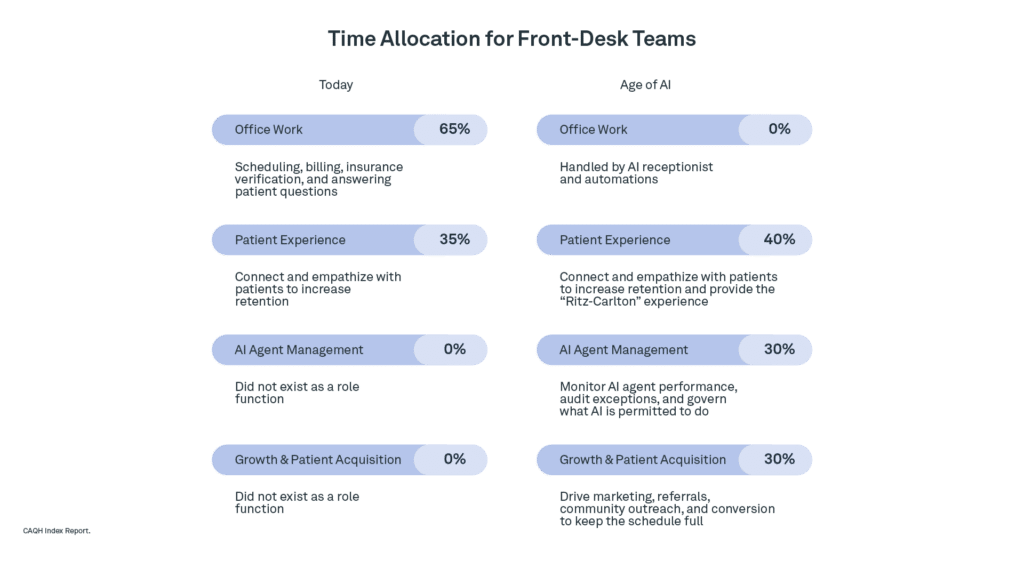

Total practice employment may hold roughly steady, especially given chronic shortages of administrative and clinical support staff. What changes is the shape of the work. Headcount per dollar of revenue falls over the decade even as practices get larger, busier, and serve more patients. The human role that used to be defined by phones, forms, and follow-up is refocused on three responsibilities:

- Hospitality. When AI removes the administrative friction, the in-person experience becomes the differentiator. Front office teams will be the reason every patient feels known, welcomed, and cared for, and practices will compete on it the way great hotels and restaurants do.

- Managing the digital workforce. The most important new responsibility in the front office is managing the system of AI agents that run the practice. That means defining workflows, watching dashboards, reviewing exceptions, deciding what the AI is allowed to do, and knowing when to step in. The office manager of 2036 works less like an administrator and more like an orchestrator, and that job requires a deep understanding of how the practice actually operates.

- Growth. New patient acquisition becomes a much bigger deal over the next decade, and the front office owns it. Marketing, community outreach, referral programs, conversion optimization, tracking acquisition costs, and managing the practice’s local reputation. The front office becomes the practice’s growth engine, responsible for keeping the schedule full.

Time Allocation for Front-Desk Teams

13. Weave estimate based on CAQH 2023 Index Report and SRS Web Solutions data

What This Means for Hiring, Training, and Pay

The traditional hiring profile favored candidates who knew the practice management system, understood insurance, and could survive the daily administrative volume. That skill set was never the problem; the volume was.

The new profile favors backgrounds in operations, hospitality, customer success, sales, and marketing. Many of those hires will come from outside healthcare entirely: hotel groups, retail management, customer experience teams. Tenured office managers become more valuable, since they’re the ones who know the practice well enough to design the workflows the AI agents run.

Compensation follows the responsibility. Expect front office pay to grow 30 to 40% beyond inflation over the decade as the role expands, with bonus structures tied to patient acquisition, satisfaction scores, and operational performance.9 Group practices will build centralized training programs covering AI agent management, growth, and hospitality — a natural extension of the technology standardization we cover next.

The paradox of the next decade is that the more agents you put to work, the more human your practice feels. The practices that treat this new era as an opportunity to grow, not cut, their people, will win every metric.

Prediction 2: Standardizing Your Technology Stack Becomes Nonnegotiable

If you run a multi-location organization, here’s the uncomfortable truth about the next decade: your size is both your greatest advantage and liability.

Scale comes with real advantages. You can centralize administrative work, negotiate better pricing with vendors and payers, and fund technology investments that a solo practice can’t afford. But scale is also why the industry has been promising operational integration for a decade and struggling to deliver it. Every acquired location arrives with its own practice management system, its own billing tools, its own imaging software, and its own habits. While group practices moved aggressively to centralize billing, contracting, HR, and procurement, the technology inside each practice was too often a holdover from whatever the original owner was using the day the deal closed.

Fragmentation was tolerable when software was just a line item. Now that AI has turned technology into the biggest efficiency opportunity a practice has, running every location on different systems means leaving that opportunity on the table.

Why Standardization Stalled

Three forces made standardization unusually hard in practice-based healthcare:

- Sellers were promised they wouldn’t have to change. During the acquisition wave of the late 2010s and early 2020s, the fastest way to close a deal was to promise owners they’d keep running things their way, and that promise usually extended to the systems the practice ran on. Forcing a tenured owner off the software they’d used for 15 years was often a deal-breaker.

- Practice software is tied to clinical identity. A provider’s system of record is where their patient relationships, treatment histories, financial arrangements, and clinical preferences live. Many providers and their staff have spent their entire careers in a single software environment, and asking them to switch feels like a threat to the continuity of their patient base. Historically, operators have chosen not to fight that attachment.

- Migration was genuinely risky. Practice data is messy: decades of records, custom codes, idiosyncratic charting conventions, and integrations to legacy hardware. Migrating it has historically meant weeks of downtime and real risk of clinical or billing errors. For an organization running on thin margins, a botched migration often costs more than fragmentation did. The result was technological gridlock: everyone knew it was suboptimal, and nobody thought it was worth fixing.

The cost of that gridlock shows up in lost efficiency. 68% of practices aren’t running on an integrated software stack, and nearly half of all practices lose at least an hour per week to software issues.8 Across an organization with dozens of locations, those hours add up to hundreds of thousands of dollars in lost productivity every year.

Why Integration is Do or Die

With the rise of AI, the cost of staying fragmented is increasing while the cost of fixing it is collapsing. It’s never been more important to shift your workflows, and never easier to do it. Here’s why:

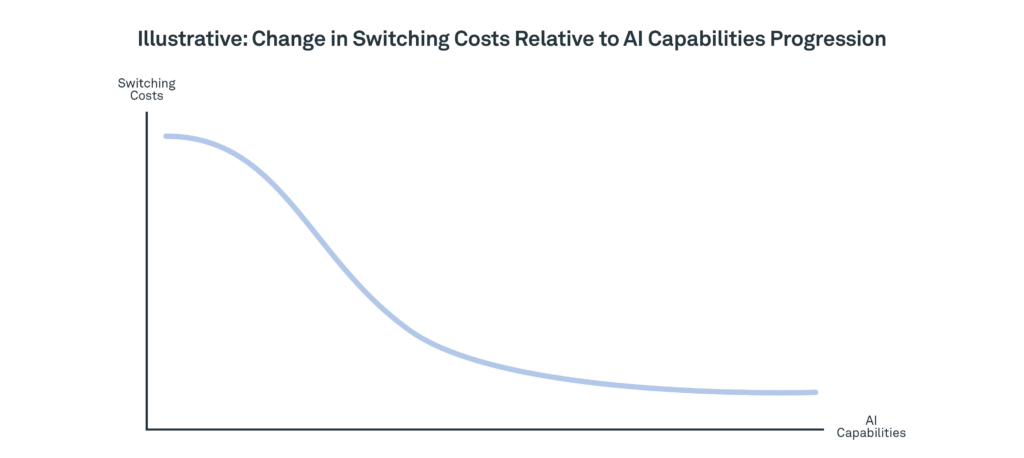

AI is dissolving switching costs. The painful part of changing systems has always been extracting, transforming, and loading messy clinical data: unstructured notes, proprietary formats, legacy schemas. AI-assisted migration tools now sit atop disparate systems, extract discrete clinical data from unstructured notes, map terminology across systems, reconcile code mismatches, and scan for errors and duplicates. What used to require a six-figure consulting engagement and weeks of downtime can increasingly be handled in a fraction of the time and cost.

Interoperability standards are maturing fast. The 21st Century Cures Act contained information-blocking provisions that forced software vendors to open their architectures — and the industry responded. Fast Healthcare Interoperability Resources (FHIR), the standard that lets healthcare systems exchange data cleanly, has reached 98% adoption among U.S. hospitals, one of the fastest standard adoptions in healthcare history.14 Practice-based verticals lag behind hospitals, but they’re following fast: the share of dental practices able to send structured treatment plans to another system jumped from 12% in 2022 to 68% by mid-2025.15

The economics compound. When every location runs the same systems, the work only has to be built once. After that, every new location inherits the benefits at almost no added cost. Centralized reporting becomes possible. AI tools are trained, governed, and deployed across the network rather than being reconfigured on a per-location basis. Vendor pricing improves, staff training becomes portable, and compliance audits become manageable. And the staffing efficiency gains from Prediction 1 are only fully achievable in a standardized environment, because AI agents can’t replace administrative labor at scale when every location runs different software.

Governance risk is climbing the agenda. 58% of practices currently operate without any AI governance structure, and fewer than one in 10 have documented, enforced policies.8 For an organization running AI across dozens or hundreds of locations on different stacks, that risk multiplies with every location. Standardized technology is what makes governance possible: auditable, secure, and defensible in front of payers and regulators.

Illustrative: Change in Switching Costs Relative to AI Capabilities Progression

As Ryan Paskin, a private equity operator in the dental space, puts it: “The winners will standardize systems, harmonize processes, and build one culture.”16

What Standardization Means for Your Vendors

This shift toward standardization transforms the software market you buy from, and it’s important to understand how.

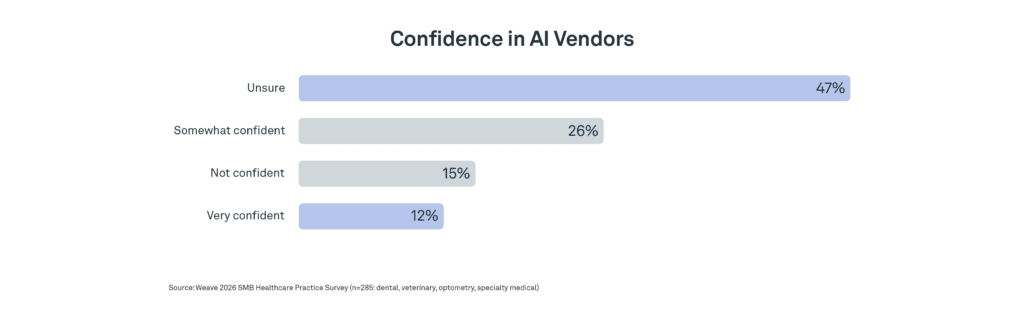

The stakes go up on both sides. In a fragmented market, losing one office is a contained loss for a vendor. In a standardized one, losing a single location can mean losing the entire organization, and winning one can mean winning hundreds. That gives multi-location buyers real negotiating leverage, and it forces vendors to grow up and provide enterprise sales teams with deeper security reviews, serious compliance documentation, and customized implementation that makes everything work. The bar is currently low. In our survey, just 12% of practices say they’re very confident in the AI vendors serving their industry, and nearly half say they’re unsure.8 Vendors that can actually earn that confidence will take share fast.

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

The ecosystem consolidates. The current market features hundreds of point solutions across communication, payments, marketing, revenue cycle, AI receptionists, and clinical documentation. As organizations standardize, the number of vendors any one of them will tolerate shrinks dramatically. Many point solutions get acquired, displaced, or squeezed out. The vendors that remain will be fewer and more enterprise-grade.

Interoperability wins. Vendors face a defining choice between two strategies. The first is the closed-loop ecosystem: a single vendor bundling the system of record, scheduling, payments, communications, and AI into one sealed suite. It’s clean and commercially simple, but no single vendor can be best-in-class in every category, and it forces buyers into a high-stakes bet on one roadmap during the fastest-moving technology cycle in memory. The second is deep interoperability: doing a few things exceptionally well and integrating reliably with everything else the organization chooses. What separates the two strategies is connection, not product count. A platform can offer several products and still run the interoperability play, as long as it plugs into the systems the practice already trusts instead of demanding to replace them.

We expect interoperability to win, and the reason is structural. For most of the software era, the moat belonged to the system of record. Once your data lived there, ripping it out was nearly impossible, because the real value was in the hundreds of workflows built on top of it. In an AI-driven environment, those workflows increasingly run above the system of record, in the orchestration layer that manages, routes, and governs AI agents. The lock-in moves from the data to the permissions, governance, and audit trails around what agents are allowed to do. Sophisticated organizations can’t afford mediocrity in any module. The pace of AI innovation punishes closed systems, and the ability to swap in better components becomes enormously valuable when capabilities improve every 12 to 18 months.

Here’s what all of this means when you’re the one signing the contract. When you evaluate vendors over the next few years:

- Look for the ones that do a few things exceptionally well rather than everything adequately.

- Ask how many systems they integrate with today, and how deeply.

- Ask for enterprise-grade evidence: security reviews, compliance documentation, and implementation support that scales beyond a single location.

- Ask how their AI is priced, and whether they can answer the cost questions in the CFO primer below without flinching.

- Weigh whether they could credibly orchestrate your stack, because a vendor that can only defend its own suite has a very different incentive structure than one that wins by making everything you own work together.

Knowing that this is where the vendor landscape is heading gives you negotiating leverage; use it.

You’ll Need a Real Technology Leader

The technology decisions a multi-location organization makes over the next decade will be among the most consequential in its history. And the truth is, most aren’t structured to make them well.

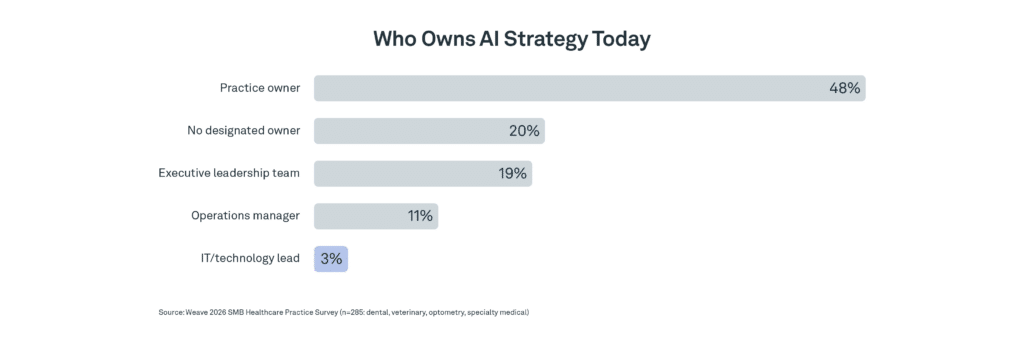

Today, where technology leadership exists at all in practice-based healthcare, it usually looks like an IT director: uptime, hardware, vendor management, break-fix support. The survey data makes the gap plain: only 3% of practices have an IT or technology lead who owns AI strategy. Nearly half say the practice owner carries it, and 1 in 5 say nobody does. The next decade requires something different. The technology executive of 2036 sits at the strategy table and owns decisions spanning vendor strategy, AI governance, data architecture, and enterprise integration. The role evolves in four ways: from infrastructure to strategy, as standardization roadmaps become board-level decisions; from technology evaluator to AI governance executive, accountable for what autonomous agents are allowed to do and how their actions are audited; from cost center to growth lever, responsible for converting technology into measurable financial outcomes; and from operator to dealmaker, because the speed of post-acquisition technology integration becomes a primary driver of deal returns.8

8. Weave 2026 SMB Healthcare Practice Survey (n=285)

The organizations that build this role early will find themselves years ahead of those that keep trying to make their biggest strategic decisions through a toolbox designed to fix printers.

Prediction 3: The Unit Economics of Your Practice Will Change

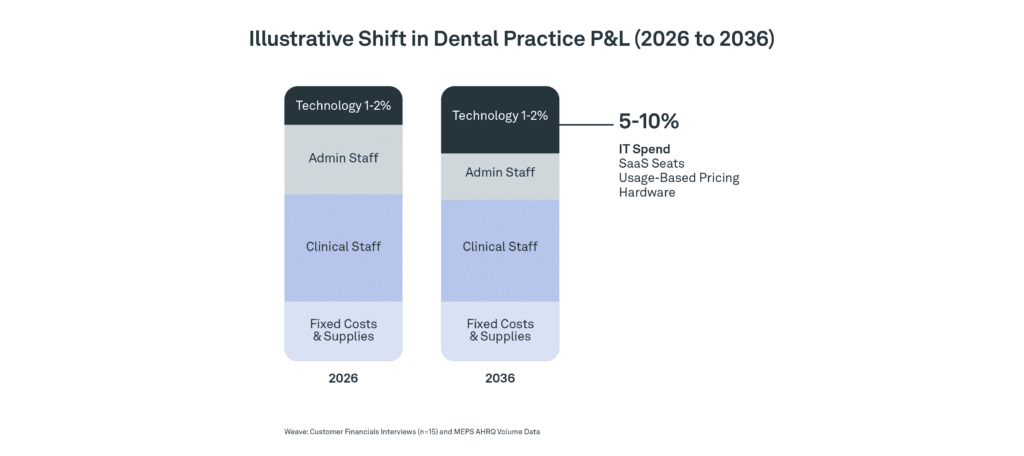

The financial model of a healthcare practice has been remarkably stable for decades. Roughly 25 to 40% of revenue goes to clinical and administrative labor, 10 to 15% to supplies and lab work, 7 to 10% to occupancy, and the rest to marketing, software, and other overhead, leaving a margin that historically hovered around 30% and has compressed to roughly 22% in dentistry.

The P&L of 2036 changes in shape as much as in size, and two structural shifts define it.

The Cost Side: From Labor-Heavy to Software-Heavy

Staff compensation is the single largest expense in a practice today, accounting for more than 40% of total overhead. As AI agents absorb scheduling, intake, verification, recall, and billing follow-up, and practices stop backfilling roles that automation covers, software spend rises to fill part of the gap. AI receptionists, clinical documentation, revenue cycle automation, diagnostic imaging, and orchestration platforms all carry real costs. The practice software line item, historically 2 to 3% of revenue, is likely to reach 6 to 9% over the next decade.10

The trade works because AI agents don’t draw benefits, payroll taxes, or replacement hiring, and their cost scales with usage rather than headcount. For a practice operating at today’s compressed 22% margin, rebuilding the cost base this way could restore margins to 28 to 32%. For multi-location organizations, where the effect compounds across every location, this is the largest operating-leverage opportunity available anywhere on the P&L.

Illustrative Shift in Dental Practice P&L (2026 → 2036)

10. Weave Customer Financials Sample Data and Internal Analysis

The Revenue Side: From Corrective to Preventive

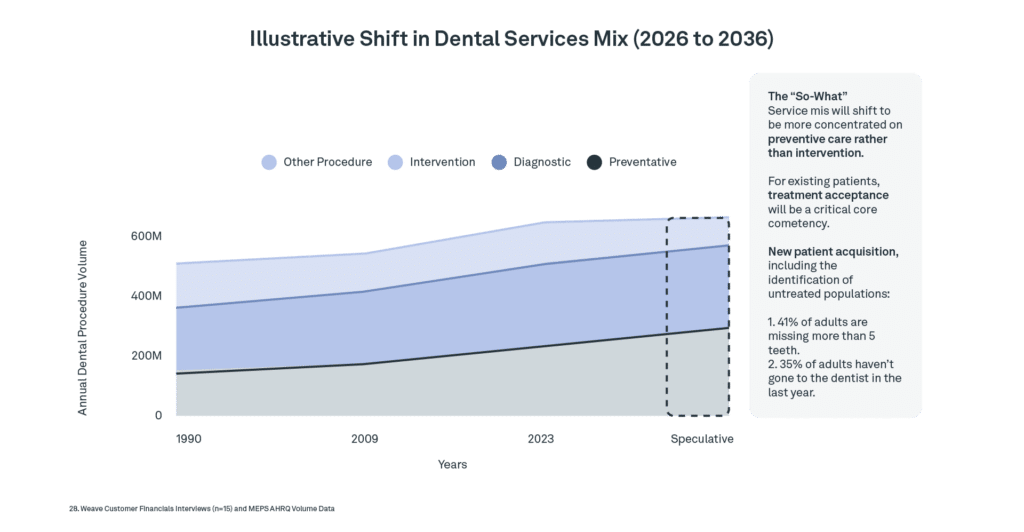

The second shift is subtler and more interesting. As AI diagnostics become standard, practices will catch problems earlier. In dentistry, a cavity caught at its earliest stage needs a small filling instead of a crown. Early periodontal inflammation gets managed with scaling and hygiene protocols instead of surgery. The same pattern is already visible across healthcare: veterinary wellness plans built on early screening, optometry practices catching disease at routine exams, specialty practices shifting toward monitoring and maintenance.

Early intervention is unambiguously better for patients. It also raises an honest question for owners: if the service mix tilts toward smaller, earlier, less invasive procedures, does that hurt revenue?

Revenue per visit will likely decline modestly. Total revenue and lifetime patient value will almost certainly rise. There are four reasons for this:

- Throughput rises. Preventive and early-intervention visits are shorter and simpler than restorative work. A practice that historically ran 8 visits per chair per day can run 10 to 12 once the mix tilts toward prevention, partially or fully offsetting lower revenue per visit.

- Lifetime value rises. Patients who experience early intervention stay healthier, stay loyal, and refer. The patient who avoids a painful root canal because their dentist’s AI caught the problem early tells five friends and stays for 15 years.

- Payer economics shift. Reimbursement has historically been transactional and procedure-based, which rewarded corrective care. The broader healthcare industry is moving toward value-based models that pay for outcomes, and practice-based verticals will follow. Over the next decade, payers will increasingly reward practices that can demonstrate strong preventive outcomes. The forward-thinking organizations are positioning their data and outcomes reporting now, so they’re ready when those payer conversations arrive.

- Acquisition matters more. A practice completing more, shorter visits needs more patients to fill the schedule, which is exactly why the front office becomes a growth engine in Prediction 1. The good news is the pool is enormous. In dentistry alone, roughly 35% of Americans, over 100 million people, get no oral care at all in a given year.17

Illustrative Shift in Dental Services Mix (2026 → 2036)

Dental Procedure Volume in Counts of Instances by Year

18. MEPS AHRQ Volume Data for 1999-2024 and Weave internal projections

Two related shifts follow. Practice membership plans and subscription plans become far more viable once AI agents handle the recurring billing, eligibility, and reminder work that made them administratively expensive, which matters enormously for the growing population of patients without traditional insurance; veterinary practices have already proven the model with wellness plans. And provider economics change: as clinical AI advances from documentation to imaging to assisted procedures, provider productivity rises, meaning practices support more throughput without proportionally growing their largest compensation line.

Budgeting for the AI Era: A Primer for the Practice CFO

Most practice owners and finance leaders built their careers on traditional software economics: flat license fees, predictable contracts, modest annual increases. AI changes that, and understanding how it’s priced will become a core skill of the practice finance function.

Most AI applications carry costs at two levels. The first is the license fee, a predictable subscription that buys access to the platform. That part looks familiar. The second is usage-based inference cost. Every time an AI model processes information (reading an insurance card, drafting a clinical note, holding a phone conversation with a patient), it consumes a measurable unit of computation called a token. AI vendors pay their underlying model providers based on tokens consumed and pass some or all of that variable cost to customers. A practice that uses its AI receptionist twice as much in a busy month pays more than in a slow one, sometimes meaningfully more.

Inference costs have been falling fast, with some estimates showing commodity token costs down nearly 90% over two years, and the trajectory continues downward.19,20 But savings don’t automatically flow to you. Usage grows as capabilities expand, so your actual cost trajectory depends on how you deploy the tools.

For budgeting, AI costs fall into three buckets that deserve separate planning:

- Platform and license fees. Predictable, fixed subscriptions for the tools you run. Budget line by line, knowing vendor pricing in this category is still maturing and will consolidate.

- Usage and inference costs. Variable costs that scale with use. For bounded workflows like insurance verification, scheduling, and documentation, these stay manageable. For high-volume workflows like outbound patient calling, they can grow quickly if nobody’s watching. Model expected usage, set caps where appropriate, and review monthly.

- Implementation and governance costs. The bucket everyone misses. Deploying AI requires integration work, staff training, change management, vendor management, security review, and increasingly, governance infrastructure. These costs often equal or exceed the first-year software cost itself.

Over the next few years, every practice finance leader should be able to ask vendors and internal teams a few pointed questions. All-in, what does one AI-completed workflow actually cost us? Does our per-use cost rise, fall, or hold flat as volume grows? What governance and compliance overhead is required, and who owns it? How do our AI costs benchmark against similar organizations? What’s our exit plan if a vendor’s pricing changes? Are we paying for capabilities we don’t use?

These are questions of financial discipline, and the finance leaders who get fluent in them early will manage this transition far better than those who treat AI procurement like any other software purchase.

The Valuation Kicker

Everything above compounds into one final implication: value. In adjacent industries, software-heavy operating models trade at notably higher multiples than labor-heavy ones. A practice or group that has shifted its cost base from labor to software, pushed margins from 22% back above 30%, and built a well-governed, AI-orchestrated operating model is simply a higher-quality business, and it commands a different multiple in any future transaction.

This is also where the size paradox resolves. Scale only pays if the operating model earns it. The gap between AI-adopting and non-adopting practices will widen substantially over the next decade: adopters running at structurally higher margins, seeing more patients, retaining their staff, and commanding stronger valuations, while non-adopters keep running the labor-heavy, corrective-heavy model under mounting pressure. Once that gap opens, it becomes very difficult to close.

Conclusion: A Different Industry, A Better One

By 2036, the practice looks structurally different from today’s. Ownership will keep shifting toward group models. Front office teams will trade busywork for hospitality, orchestration, and growth. Technology stacks will standardize, and the organizations buying software will demand more from fewer vendors. The economics of running a practice will be rebuilt, with software carrying more of the cost base and prevention carrying more of the revenue.

The pace will vary by region, vertical, and organizational maturity, but the direction is already set, and the underlying trends are underway. This is an opportunity for practices to choose the operating model that will define the next generation of care while your competitors are still deciding whether to take any of this seriously.

And the most important prediction is the least flashy one: as AI takes on more of the administrative work, healthcare gets the chance to become more human. Less time buried in screens and forms means more time for the conversations, the reassurance, and the care that made people choose this profession in the first place. That’s a future worth building toward.

Curious how your practice compares to the 285 we surveyed? Let’s talk about where your operation stands, from staffing and automation to AI readiness, and what these predictions mean for you.

Talk to our team>

Endnotes

- ADA Health Policy Institute. “Net Income / Gross Billings.” Survey of Dental Practice. American Dental Association, 2025.

- Vujicic, Marko et al. “An Analysis of Dentists’ Incomes, 1996–2009.” Journal of the American Dental Association 143, no. 5 (May 2012): 452–460.

- ADA Health Policy Institute. “Trends in Dentists’ Income, Revenue, and Hours Worked.”

- ADA Health Policy Institute. “Net Income / Gross Billings.” Dental Practice Research, 2025.

- Becker’s Healthcare Research & Clerri. “How DSOs Are Tackling the Profit Squeeze.” White paper, 2024.

- Education Data Initiative. “Average Dental School Debt.” https://educationdata.org/average-dental-school-debt

- Weave Dental Market Sizing Analysis.

- Weave 2026 SMB Healthcare Practice Survey (n=285).

- Weave Strategy Team Internal Analysis.

- Weave Customer Financials Sample Data and Internal Analysis.

- Analysis informed by Anthropic research, Weave surveys, and internal calculations.

- Weave Key Opinion Leader (KOL) Primary Interviews (n=12).

- Weave estimate based on CAQH 2023 Index Report and SRS Web Solutions data.

- HL7 International. 2025 State of FHIR Survey Results.

- Mordor Intelligence. “Dental Practice Management Software Market Size & Share Analysis.” Mordor Intelligence. Accessed July 10, 2026. https://www.mordorintelligence.com/industry-reports/dental-practice-management-software-market.

- PitchBook Annual US Private Equity Breakdown for 2025.

- Cigna Healthcare. Dental Trends Report 2025. Cigna Healthcare, 2025. As reported in “35% of Americans Have Not Visited the Dentist in More Than a Year.” Becker’s Dental Review, August 13, 2025.

- MEPS AHRQ Volume Data for 1999–2024 and Weave internal projections.

- Guido Appenzeller. “Welcome to LLMflation: LLM Inference Cost Is Going Down Fast.” Andreessen Horowitz, November 12, 2024.

- Ben Cottier, Ben Snodin, David Owen, and Tom Adamczewski. “LLM Inference Prices Have Fallen Rapidly but Unequally Across Tasks.” Epoch AI, March 12, 2025.

Additional Notes

Key Opinion Leader (KOL) Interviewee Bios

Amy Manzo, Senior Director of Operations, MB2 Dental. A former dental practice owner who transitioned from clinical ownership to high-level operations, Amy now oversees a large network of practices for MB2 Dental. Her expertise lies in decentralized management, bridging clinician autonomy and corporate operational excellence.

Brian A. Colao, Director of the Dental Service Organizations Industry Group, Dykema. A preeminent legal authority in the group-practice space with over 25 years in healthcare regulatory matters and complex M&A. He pioneered the legal landscape for dental support organizations and serves on the Board of Directors for Women in DSO.

Dr. Cindy Roark, Senior Vice President & Chief Clinical Officer, Sage Dental. A clinical leader with a Master of Science in Healthcare Management from Harvard and a dental degree magna cum laude from Boston University. Her career includes practice ownership, faculty leadership at Vanderbilt University Medical Center, and Chief Clinical Officer roles at two national dental organizations.

Debbie Evans, DAADOM, Practice Administrator, Wainright & Wassel, DDS. A practice administrator with nearly 30 years of experience, holder of Diplomate status from the American Association of Dental Office Management, and 2020 National Practice Administrator of the Year.

Dr. Emily Letran, CEO & Entrepreneur, Exceptional Leverage Inc. A clinician and high-performance business mentor who has owned and operated multiple multi-specialty group practices in Southern California for over 23 years. She is a Certified High Performance Coach and TEDx speaker.

Dr. Hendrik Lai, Co-Founder, Sage Dental Consulting. An internationally recognized consultant and former dental surgeon with an MBA, EMBA, and MS in Business Analytics, and more than 15 years of management consulting experience across healthcare, finance, and technology.

Joshua Austin, DDS, MAGD, FACD, Dentist & Editorial Director, Dental Economics. A clinician and educator holding Mastership status in the Academy of General Dentistry, a distinction held by fewer than 2% of U.S. dentists, and a monthly columnist for Dental Economics.

Matthew McGaw, Marketing Executive & Industry Specialist. A strategic leader in the practice technology sector, currently affiliated with DSO Compass and formerly of Weave, focused on scaling technology adoption across multi-location healthcare organizations.

Roshan Parikh (Dr. Ro), Founder & CSO, DSO Strategy LLC. A clinician-turned-operator who built a single practice into a 35-office group with $60M+ in annual revenue through a successful private equity exit, and the former Head of Dentistry for Walmart Health.

Ophir Tanz, CEO, Pearl. Ophir is an award-winning entrepreneur and technologist with over two decades of experience building AI-driven companies, advancing computer vision innovation, and scaling category-defining technologies to global impact. Prior to founding Pearl, Ophir was the founder and CEO of GumGum, an applied computer vision company focused on the media category. Prior to this, Ophir was CEO and co-founder of Mojungle.com, a mobile-media sharing platform that was sold to Shozu.com in 2007. Before this, Ophir co-founded and sold Fluidesign, an interactive and branding agency. He holds a BS and MS from Carnegie Mellon University.

Ben Plomion, COO, Pearl. [With over two decades of experience in marketing, commercial and operational leadership across Artificial Intelligence, Computer Vision, and Blockchain, Ben Plomion is the Chief Operating Officer at Pearl—the leading AI Software-as-a-Service (SaaS) company in dentistry. Prior to Pearl, he served as Chief Marketing Officer at Dibbs, an Amazon-backed tokenization-as-a-service (TaaS) platform. He was previously Chief Growth & Marketing Officer at GumGum, where he played a pivotal role in advancing AI-driven contextual advertising. Earlier in his career, Ben led global digital media efforts at both Magnite and GE Capital. A Forbes contributor and trusted advisor to companies like Deanna.ai, PebblePost, and #Paid, he is also a committed educator in the realms of AI, marketing, and Web3.

Chris Moxon, Managing Partner and Leader for Global Dental Practice, Boston Consulting Group. Christopher is a Managing Director and Partner in the Boston office of BCG. He is part of the Principal Investors & Private Equity (PIPE) Practice Area. He leads BCG’s Dental Provider topic in North America, advising on growth strategy, market diligence, and value creation for dental service organizations (DSOs) as well as across the broader dental ecosystem. He works closely with private equity investors and management teams to identify opportunities to scale platforms, improve practice-level performance, and drive sustainable growth.

Table of contents

Get the best of Weave, right in your inbox.

More Like This

Ready to grow your practice?

See firsthand how Weave can help you grow your practice.